A very different US business cycle

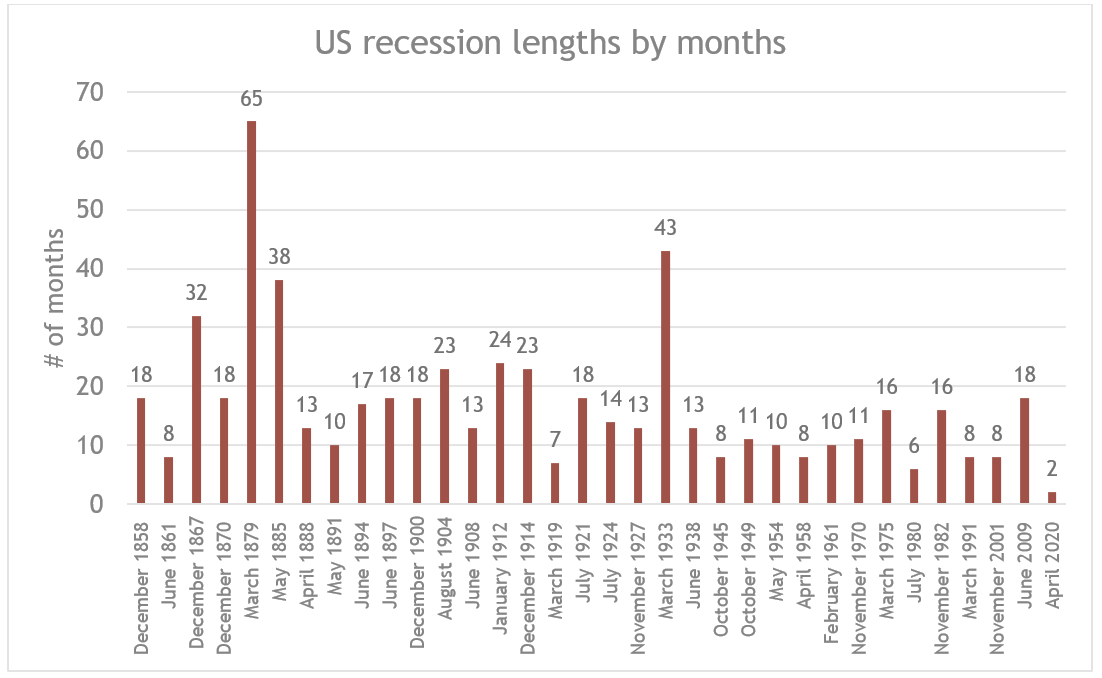

In spite of some dire predictions at the start of the pandemic, the Covid-led recession has been the shortest in US history. It lasted just two months, compared with 18 months for the Global Financial Crisis (GFC) or an astonishing 43 months for the Great Depression. This speedy recovery is welcome but suggests we may be further along in the business cycle than in a ‘normal’ recovery.

In spite of some dire predictions at the start of the pandemic, the Covid-led recession has been the shortest in US history. It lasted just two months, compared with 18 months for the Global Financial Crisis (GFC) or an astonishing 43 months for the Great Depression. This speedy recovery is welcome but suggests we may be further along in the business cycle than in a ‘normal’ recovery.

Source: NBER/Smith & Williamson Investment Management LLP, Data as at 05/08/2021

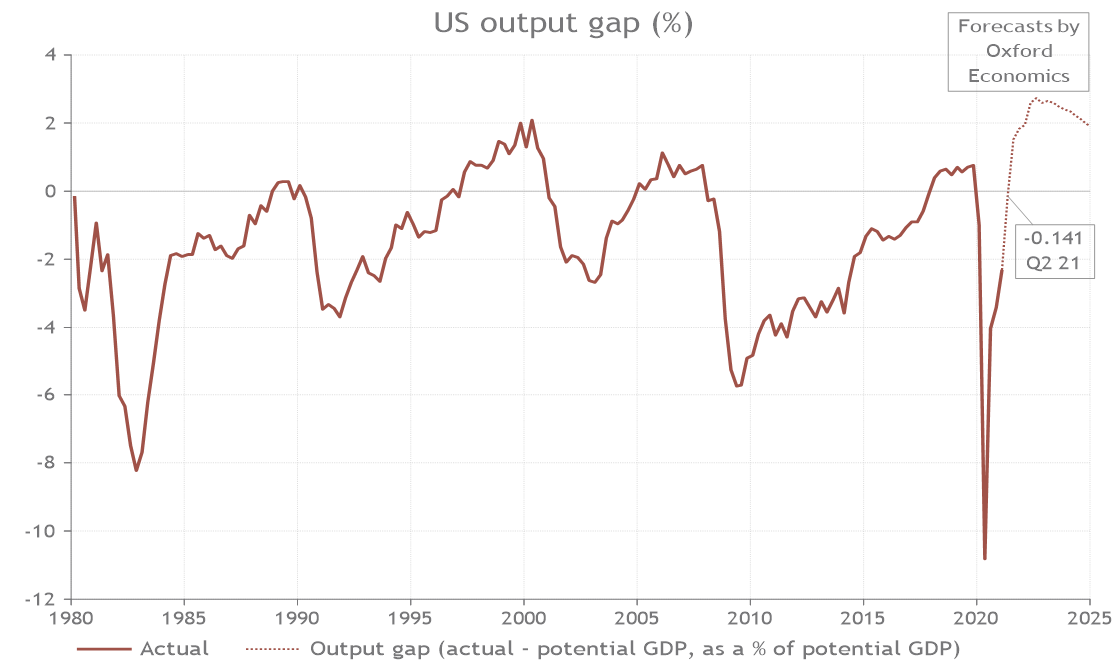

Overall, the US economy normally takes time to recover back to its pre-recession trend. In this cycle, we could be there already. It has been the fastest rebound in real US GDP in history, albeit after a significant contraction, and stands in significant contrast to the GFC. There are many factors that have made the difference, including fiscal stimulus, which has helped preserve jobs and spending. Above all, the key factor may be the nature of the crisis – more akin to a natural disaster than a ‘normal’ recession that was driven by Fed tightening and/or over leverage that takes time to unwind.

With this brief recession now over, US retail sales are now at levels that the pre-recession trend suggested wouldn’t happen until 2026.1 US house prices have soared. The labour market is tightening. The measure of ‘quits’ – those people leaving their jobs by choice – is near record highs. People don’t tend to leave their jobs if the labour market is weak. At the same time, worker shortages are at all-time highs.

The output gap (the difference between actual GDP and potential GDP, as a % of potential GDP) has likely closed already and probably at its quickest rate in history. To put this in context, it is six or more years ahead of post-GFC recovery. Many sectors in the US economy are significantly ahead of where they usually are at this stage of the cycle. It may be that while it still feels like the early days of the recovery, it is, in fact, increasingly mature.

Source: Refinitiv Datastream/Smith & Williamson Investment Management LLP, Data as at 05/08/2021

The US economy is well ahead of other countries for the time being, but other countries are catching up fast. GDP for the UK and France are around -3% below pre-pandemic levels, while Spain and Italy are lower, but significant economic growth is forecast for the year ahead as countries open-up from lockdowns2. Other countries such as Germany are only marginally behind the US.

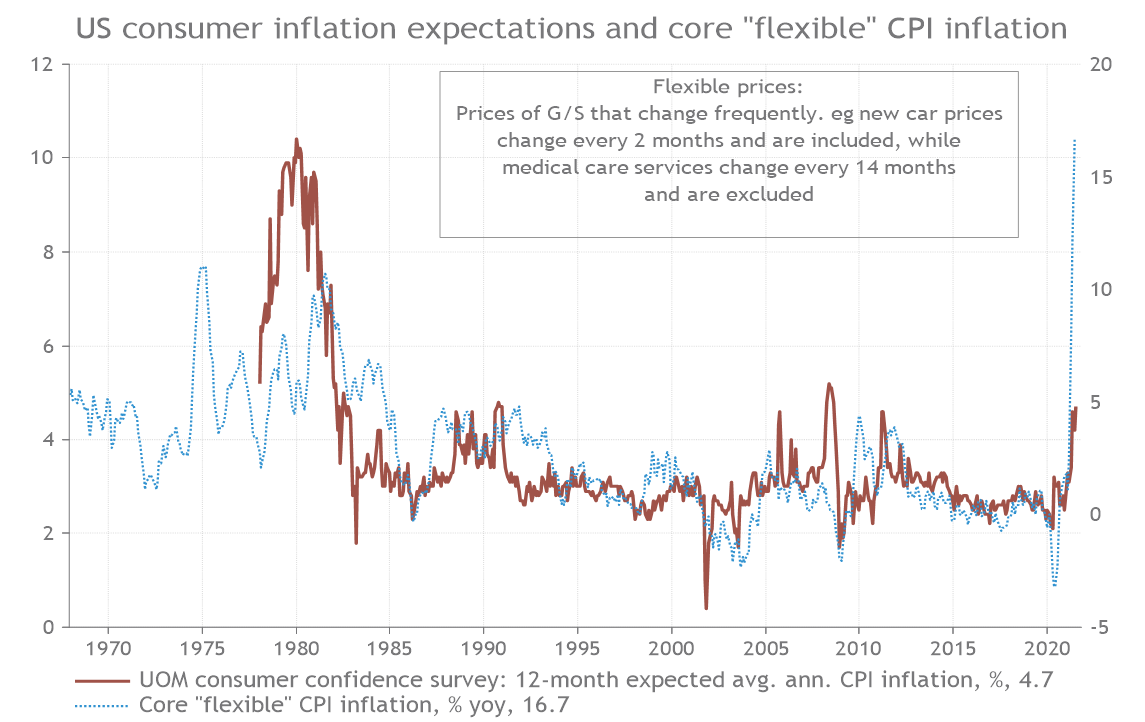

Inflation is making a comeback

This accelerated business cycle has implications for inflation. Consumer price inflation has increased globally, and particularly in the US, where June underlying core (ex-food/energy) inflation accelerated to a 4.5% annual rate, its fastest clip for 30 years3. Breaking down the core inflation further we are seeing record “flexible” CPI inflation. These are goods and services where the prices change frequently. This includes new car prices, which change every two months, but excludes medical care services, which change every 14 months. The latest data shows that US core flexible CPI inflation rose 16.7% from a year ago, even higher than a previous peak of 11% during the inflationary 1970s4. Given that flexible prices are closely correlated to surveys of consumer inflation expectations, this suggests that inflation is becoming increasingly ‘unanchored’. This is important, as central bankers throughout history have emphasised the importance of pricing predictability – ‘anchored’ expectations. Unanchored inflation expectations are associated with high and difficult-to-address inflation, such as that seen in the 1970s.

Source: Refinitiv Datastream/Smith & Williamson Investment Management LLP, Data as at 05/08/2021

Asset class implications

The MSCI All Country World equity index has ignored inflation concerns and rallied 12% (GBP, total return terms) this year on the back of a global growth recovery and accommodative policy support. It appears that equities – at least those with pricing power – continue to offer good protection against inflation5.

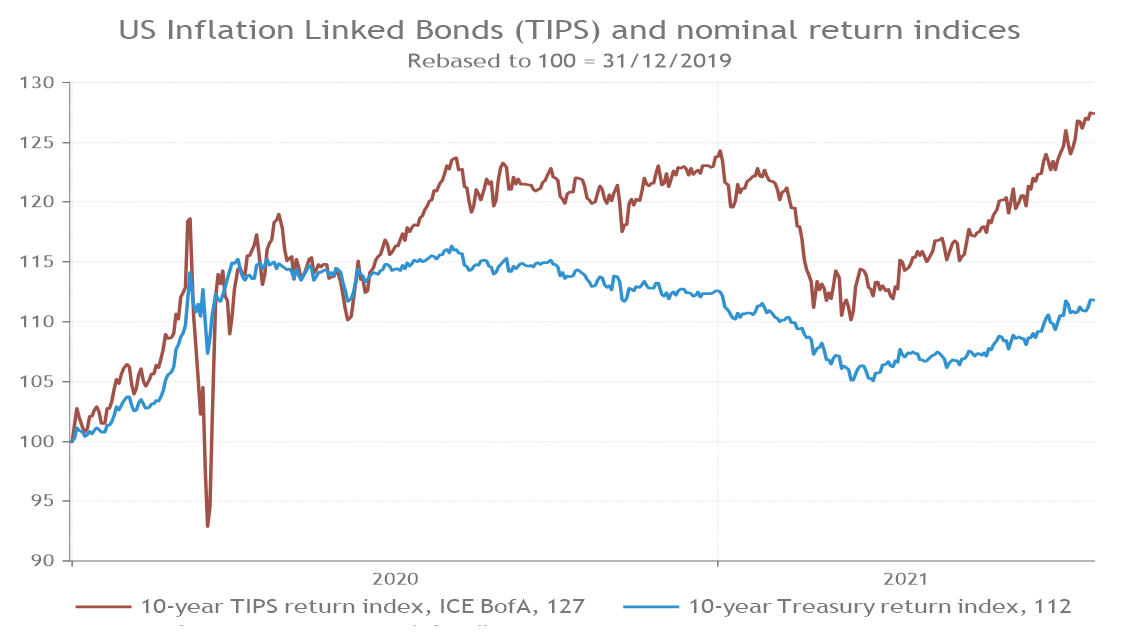

However, the same is not true of the bond markets. Treasury yields look increasingly disconnected from inflation – yields are still falling even as inflation pressures rise. It is possible that yields have been anchored down by technical factors related to money flows into the US bond market (the world’s largest). For instance, Treasury demand has been supported by international investors adding to positions following record redemptions during the pandemic, while bond supply has been squeezed by the Fed effectively buying up all new Treasury bond issuance during the second quarter. That’s been possible as the US government has run down cash balances raised during record bond sales last year for fiscal spending. Bond yields have also been lowered by a Fed that is intent on keeping policy accommodative.

While there is certainly an argument that the Federal Reserve and other central banks will defer interest rate rises, this disconnect in the bond market is starting to look increasingly unrealistic. Either way, this suggests potential risks are building in fixed income markets. To our mind, investors are better off in TIPS and other inflation-linked bonds, like index-linked gilts in the UK, where they have more protection. Inflation-linked bonds have already started to reflect higher inflation, but we believe they may have further to run.

Source: Refinitiv Datastream/Smith & Williamson Investment Management LLP, Data as at 05/08/2021

To conclude, this is a very different business cycle and we may be further ahead than we would be in a normal cycle. Investors need to exercise real caution in assets that don’t appear to reflect the potential for higher inflation, notably in fixed income market.

Sources:

1. US recovery at 1 year. Late cycle already? Jim Read, July 2021

2-5. Refinitiv Datastream, data as of 5 August 2021

Ref: 98921eb

DISCLAIMER

By necessity, this briefing can only provide a short overview and it is essential to seek professional advice before applying the contents of this article. This briefing does not constitute advice nor a recommendation relating to the acquisition or disposal of investments. No responsibility can be taken for any loss arising from action taken or refrained from on the basis of this publication. Details correct at time of writing.

Risk warning

Investment does involve risk. The value of investments and the income from them can go down as well as up. The investor may not receive back, in total, the original amount invested. Past performance is not a guide to future performance. Rates of tax are those prevailing at the time and are subject to change without notice. Clients should always seek appropriate advice from their financial adviser before committing funds for investment. When investments are made in overseas securities, movements in exchange rates may have an effect on the value of that investment. The effect may be favourable or unfavourable.

Smith & Williamson Investment Management LLP is part of the Tilney Smith & Williamson group.

Smith & Williamson Investment Management LLP is authorised and regulated by the Financial Conduct Authority

© Tilney Smith & Williamson Limited 2021

Disclaimer

This article was previously published on Smith & Williamson prior to the launch of Evelyn Partners.