Detecting value in metals and mining stocks

It is becoming commonplace to talk of a new commodities super cycle. The last cycle peaked in 2008 after 12 years of expansion, fuelled by the rise of China and growing demand for raw materials. It seems increasingly likely that a new cycle began in mid-2020 after a 12-year contraction.

It is becoming commonplace to talk of a new commodities super cycle. The last cycle peaked in 2008 after 12 years of expansion, fuelled by the rise of China and growing demand for raw materials. It seems increasingly likely that a new cycle began in mid-2020 after a 12-year contraction. A confluence of factors, including economic recovery, policy stimulus and rising inflation expectations that bring purchases forward before they become too expensive, have been behind the recent rise in the copper price, which is a key driver of the performance of the metals and mining sector. The development of the ‘green’ infrastructure theme is also pushing metal prices higher, as supply is squeezed from lower capital investment and demand for low carbon emission technology (e.g. electric vehicles).

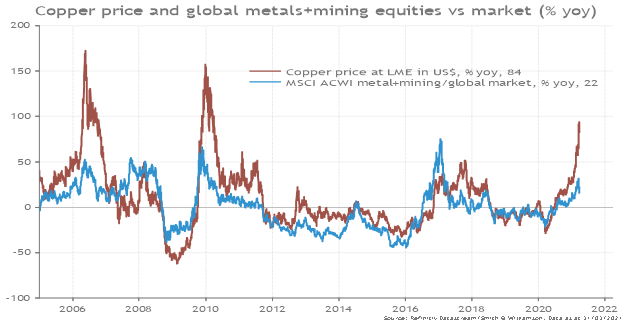

The opportunity for investors is that resource-related share prices have lagged commodity price gains. For instance, stocks in the metals and mining space are up 22% from a year ago, against an 84% gain in copper prices.1

Chart 1: Copper price gains exceeding metal and mining stock performance

Source: Refinitiv Datastream/Smith & Williamson Investment Management LLP, Data as at 31/03/2021

We look at 5 fundamental reasons why metals and mining stocks can rally on the back of rising commodity prices.

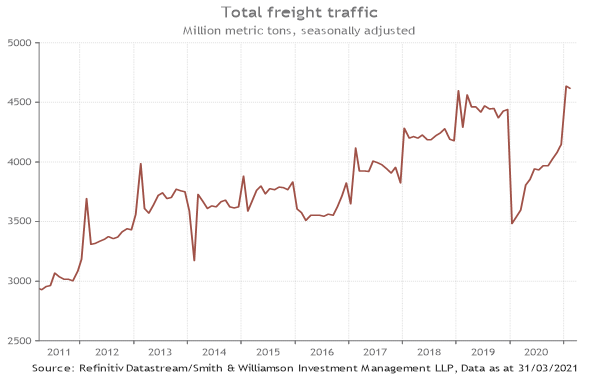

#1) China’s economic recovery: Given that China is the world’s largest end-consumer of copper, the economy’s recent impressive recovery has relevance for the metals and mining sector. While China’s macro data is heavily distorted by a low base last year from the pandemic-led lockdowns that inflates the annual data, the monthly data shows an improvement in the early months of 2021. For instance, the seasonally adjusted total freight traffic data, which measures the circulation of goods around highways, waterways and railways, is observable on a monthly basis and has steadily been recovering since a low in January 2020. Freight traffic is now 4% higher than pre-pandemic levels at the end of 2019.2 The risk here is that the Chinese authorities rein in policy stimulus on concerns of financial risks emanating from property speculation.

Chart 2: China’s economic activity is above pre-pandemic levels

Source: Refinitiv Datastream/Smith & Williamson Investment Management LLP, Data as at 31/03/2021

#2) Green infrastructure: Electric vehicle demand is growing quickly, with 2021 billed as an ‘inflection year’ for the sector. The International Energy Agency forecasts that the total electric vehicle fleet will be 60 million in 2026, a 7½-fold increase from 20193. Their growth is fuelling demand for specific commodities: battery powered electric vehicles use around 183lbs of copper, for example, compared to 48lbs for a combustion engine car4. Copper prices have already been rising on the back of this new source of demand, along with other specialist metals used in car batteries such as lithium.

Government stimulus packages and support for the energy transition are likely to boost demand for metals more generally. Green infrastructure development is metals-intensive and should create demand for aluminium and nickel.

#3) Tight supply is evident in low Chinese copper inventories: For a period of time in 2020, copper production had to be halted in many mines due to the COVID crisis and this has impacted supply. Miners are, in many cases, struggling to meet demand, particularly for certain commodities. This is evident in Chinese copper inventories being drawn to historically low levels for this time of year. Furthermore, capital expenditure among the mining companies is also low, which is constraining supply.

Chart 3: China’s copper inventory is seasonally low for this time of year

Source: Refinitiv Datastream/Smith & Williamson Investment Management LLP, Data as at 31/03/2021

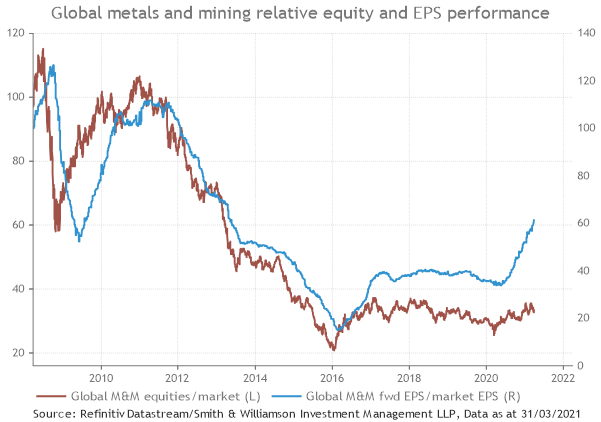

#4) Improving metals and mining Earnings Per Share (EPS) performance: The share prices for many mining companies have yet to catch up with the pick-up in relative outperformance of Earnings Per Share for the broader market seen since mid-2020. Given that metals and mining EPS has been a significant underperformer, on a relative basis, since the Global Financial Crisis more than 10 years ago, there seems to be plenty of room for EPS to recover. There are some concerns over rising input costs, although this does not look to be eroding profit margins for mining companies.

Chart 4: Relative fundamental EPS improvement supports metals and mining stocks

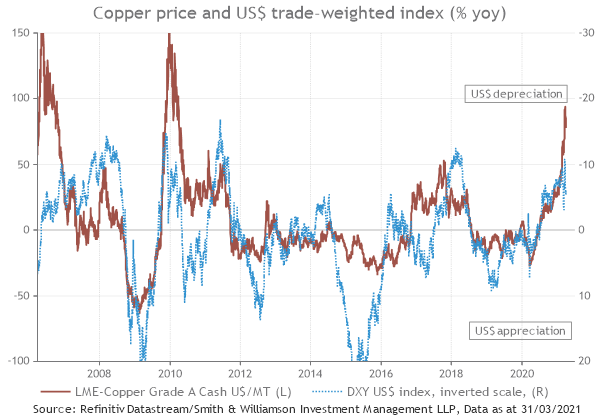

#5) USD depreciation should support rising copper prices: Copper prices typically show a high correlation with the USD. Although the USD has made modest gains so far in 2021, the greenback has depreciated 10% since last March, as rising US debts and deficits are becoming a drag on the USD5. Importantly for the metals and mining sector, a weaker USD is generally more supportive of strong copper prices and vice versa. The rationale behind the relationship is that copper is traded globally in USD, and a weaker dollar makes it cheaper in local currency terms and should therefore increase demand and affordability.

Chart 4: The downward direction of the USD supports higher copper prices

Source: Refinitiv Datastream/Smith & Williamson Investment Management LLP, Data as at 31/03/2021

A key risk to the metals and mining sector, as with many other sectors, is a resurgence of COVID cases and subsequent lockdowns. Considering the relatively slow delivery of the COVID-19 vaccine, Europe appear vulnerable to a resurgence in the pandemic and particularly its manufacturing sector, a large end-user of raw materials. However, despite the imposition of further lockdowns in continental Europe, factory output is gathering strength. In March, the Eurozone manufacturing Purchasing Managers Index reached its highest ever level of 62.4 on the back of a pick-up in global trade and the low level of finished inventory products relative to new orders6.

USD appreciation is another risk for the metals and mining sector. The USD has appreciated slightly against the major currencies on higher US growth expectations and rising long-term interest rates. Our base case is that this is more of a transitory development ahead of another leg down in the dollar, as foreign buyers have shown less appetite for US Treasury bonds against a background of recovering growth and sharply rising public debt. This appears borne out in the data. In the fourth quarter of 2020, foreign investors - who owned a peak of 57% of marketable Treasury securities in 2008 when the Fed started Quantitative Easing (QE) - have since seen their share steadily fall to 32%, the lowest ratio since 20007.

Sources:

1,2,5,6,7 Refinitiv Datastream, Smith and Williamson Investment Management LLP, data as at 31 March 2021

3 Demand for metals and materials that support renewable energy and electric vehicles will soar, What I Learned This Week, 13D, 25 March 2021

4 Copper Development Association, Electric vehicles, data as at 31 December 2020

DISCLAIMER

By necessity, this briefing can only provide a short overview and it is essential to seek professional advice before applying the contents of this article. This briefing does not constitute advice nor a recommendation relating to the acquisition or disposal of investments. No responsibility can be taken for any loss arising from action taken or refrained from on the basis of this publication. Details correct at time of writing.

Please remember investment involves risk. The value of investments and the income from them can fall as well as rise and investors may not receive back the original amount invested. Past performance is not a guide to future performance.

Notes to editors

Smith & Williamson is a leading financial and professional services firm providing a comprehensive range of investment management, tax, financial advisory and accountancy services to private clients and their business interests. The firm’s c1,800 people operate from a network of 11 offices: London, Belfast, Birmingham, Bristol, Dublin (City and Sandyford), Glasgow, Guildford, Jersey, Salisbury and Southampton. Smith & Williamson is part of The Tilney Smith & Williamson Group.

Smith & Williamson Investment Management LLP

Authorised and regulated by the Financial Conduct Authority.

Registered in England No. OC 369632. FRN: 580531

Smith & Williamson Investment Management LLP is part of the Tilney Smith & Williamson group.

© Tilney Smith & Williamson Limited 2021

Disclaimer

This article was previously published on Smith & Williamson prior to the launch of Evelyn Partners.