Enterprise Management Incentive (EMI)

An EMI is a tax-advantaged share option scheme that gives smaller listed and privately-held companies a highly tax-efficient means of rewarding, incentivising and retaining qualifying employees.

What is an EMI?

An EMI is a tax-advantaged share option scheme that gives smaller listed and privately-held companies a highly tax-efficient means of rewarding, incentivising and retaining qualifying employees. The main benefit of EMI is that employees may participate in share growth without incurring an income tax or national insurance liability and at advantageous capital gains tax rates. There may also be generous corporation tax deductions available for the employer.

How does an EMI work?

A qualifying, broadly full-time, employee is awarded options over shares in the employing company or parent company if in a group. The option documentation will specify the exercise price and when the option may be exercised. It must also specify any performance or other conditions that must be satisfied before the option is exercisable.

When conditions are satisfied, the option can be exercised at the agreed price. The employee then owns the shares and is subject to capital gains tax when the shares are sold.

EMI qualifying requirements

The main requirements for options to qualify under EMI are as follows:

|

Requirement |

Limits |

|

Maximum value of company’s gross assets |

£30 million |

|

Maximum number of full-time employees |

249 |

|

Maximum value of shares under option (company) |

£3 million |

|

Maximum value of shares under option (employee) |

£250,000 |

|

Maximum employee’s material interest |

30% of ordinary share capital |

|

Minimum employee’s working time |

25 hours per week/75% of working time |

|

Exercise period |

Must be capable of being exercised within 10 years |

There are further requirements in respect of independence, subsidiaries and qualifying trade.

Tax implications of EMI

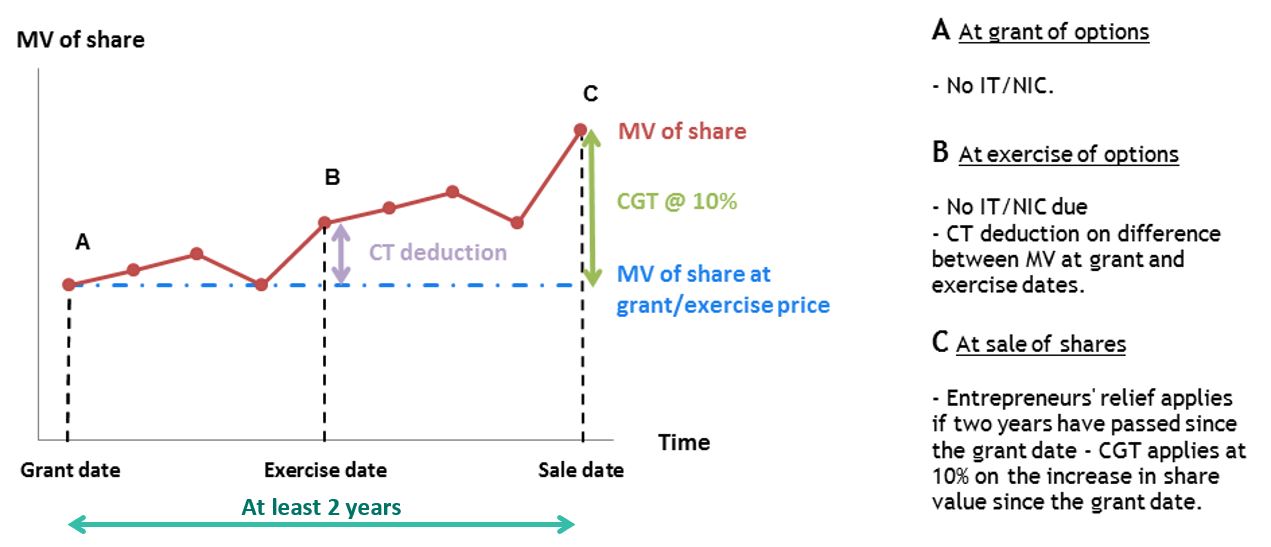

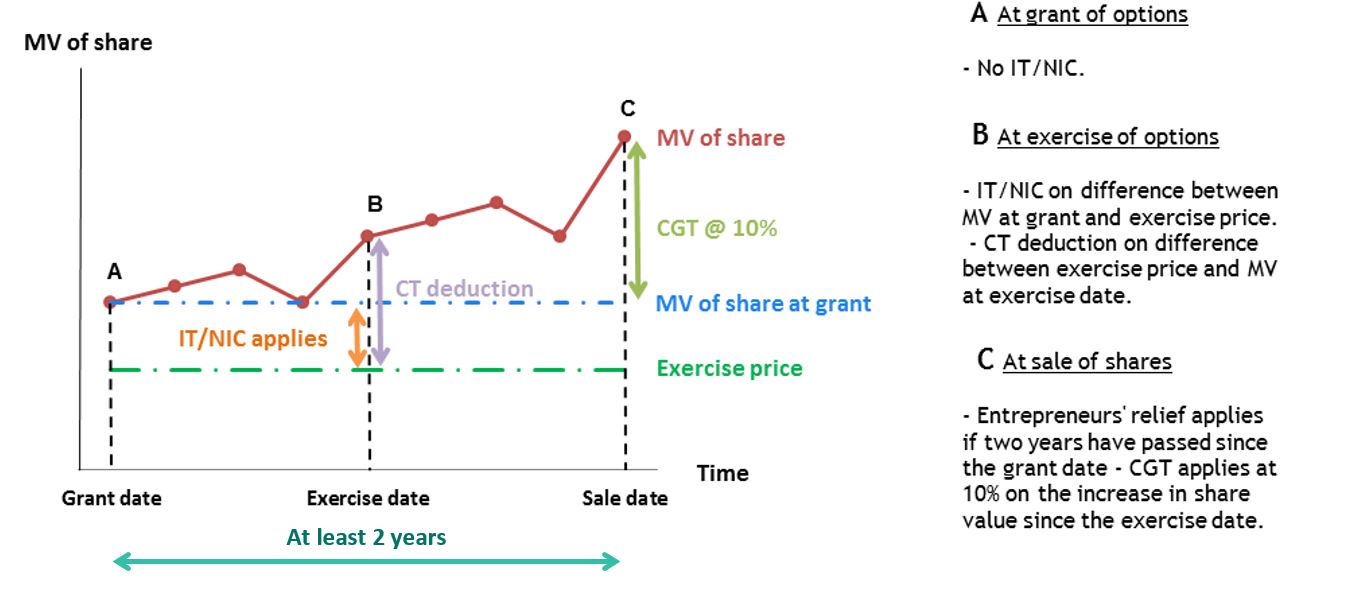

The two examples below set out the income tax (IT), NIC and corporation tax (CT) position of the EMI options at exercise, and the capital gains tax (CGT) position at sale of shares. The treatment differs if the exercise price is lower than the share market value (MV) at the option grant date.

Example 1: option exercise price = MV of share at grant

Example 2: option exercise price < MV of share at grant

How we can help

- Advising of scheme appropriate to meet company objectives;

- drafting customised scheme rules that comply with the legislation;

- preparing a tax memorandum and explanatory booklet if required;

- obtaining advance assurance from HMRC on the qualifying status of the company;

- obtaining HMRC agreement of the market value of shares at the award date; and

- assisting with online registration and all HMRC reporting requirements.

Ref: NTNPW042051

Disclaimer

This article was previously published on Smith & Williamson prior to the launch of Evelyn Partners.