How will you afford to retire?

Long-term financial commitments can take their toll. Even if you’re a high earner it’s crucial that you balance the cost of your lifestyle with saving and investing for retirement.

Long-term financial commitments can take their toll. Even if you’re a high earner it’s crucial that you balance the cost of your lifestyle with saving and investing for retirement. Failure to save enough when your income is strong could result in you having to delay the age at which you retire.

The question of how to weigh your financial commitments today with your retirement needs leads to a delicate balance even for high earners between funding education, making large mortgage payments, other discretionary expenditure, such as cars and holidays, or saving for the future.

Many underestimate the financial demands of retirement, particularly in light of increased life expectancy and the cost of care in older age.

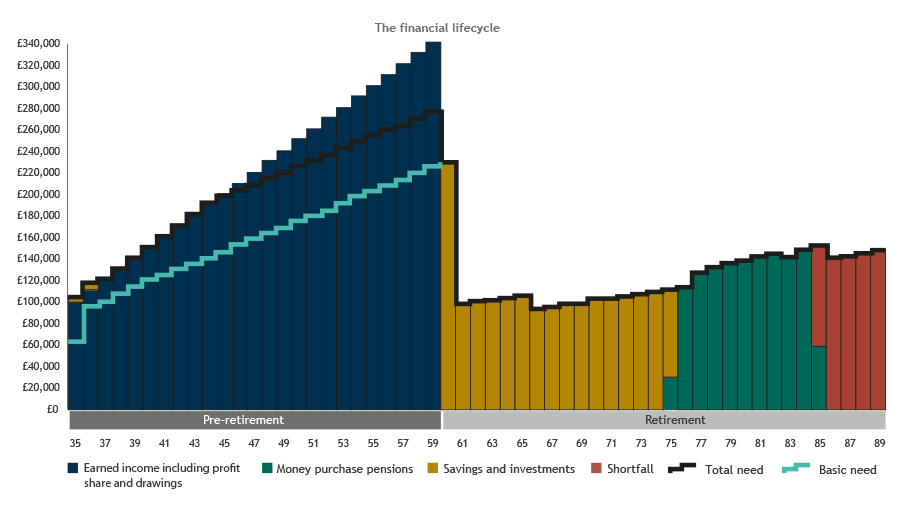

The chart above is an example projection of the financial lifecycle of a high earner, such as a young associate advancing through a professional partnership into retirement. Their financial profile is typical of many high earners in that it shows both income and expenditure steadily increasing.

It is based on a complex actuarial model to demonstrate how income and spending change during life and is one we use for our own clients to demonstrate potential outcomes from their incomes, expenditure and savings during their life.

In our example, we are assuming this individual is appointed as a partner in a law firm in their mid-30s, earning a profit share of £100,000 per annum at age 35, increasing steadily to £250,000 at age 50 and to £350,000 at age 60. The partner is married and has a non-working spouse; retirement is at age 60, which then assumes 30 years of retirement, as the life expectancy of a professional retiring in the next few years is into their 90s.

Although the couple save into ISAs each year and put money into a pension and other investments, the amounts are insufficient to carry them through retirement, forcing them into the red in their 80s.

Should the couple need care in their later years, their financial situation could worsen considerably, with the likelihood that they need to sell their home to pay for care.

The financial stress of divorce would aggravate their position.

Failure to make the necessary financial provision for retirement can frequently mean individuals need to delay the date at which they stop working. Not only is this frustrating from a personal point of view but also from a business’ perspective it can hold up the career progression of others within a firm.

Planning ahead

Financial planning should begin at a minimum in your early to mid-30s. Since April 2016, individuals with annual adjusted income over £150,000 have had their annual pension allowance reduced at a rate of £1 for every £2 earned over the threshold. Those with incomes over £210,000 a year can now only contribute £10,000 a year into a pension with tax relief.

Although the chart takes the hypothetical example of a partner in a law firm who has a set basic profit share, which steadily rises over time, the overall profile and comments are applicable to many high earners irrespective of sector.

Observations:

- Our couple dips into savings in their mid-30s, break even in the years up to age 45, and have surplus funds available to save and invest after this time.

- Income increases over time so they could have saved more from their mid-40s, but experience shows that people often fail to do this. Instead, income is often devoted to school fees, a second or bigger home, new cars and holidays.

- On retiring at 60, their savings and investments are quickly depleted as their lifestyle is not reduced sufficiently to match income. By age 75, the couple are relying on pension income to fund their expenditure.

- By age 85, the couple have exhausted their savings, investments and pensions with the exception of their main residence.

- Today, residential or nursing care often costs in excess of £60,000 per annum per person. If required in the future it might require our couple to sell the family home. In figure 1, the couple remain in their home but go into the red, as they do not have any income.

- Couples like our example may have to consider saving more when earning well, working later in life, a non-earning partner taking a job or liquidating major assets later in life.

Recommendations:

- In this case, seeking financial advice from the time of becoming a partner could have helped to mitigate the ‘cliff effect’ at retirement.

- High-earners should draw up a financial plan and review it regularly.

- If your firm offers financial education for senior people, directors or partners, take it up to help you plan properly for your retirement needs.

Notes

Assumptions made in our model include:

- Annual expenditure for the couple is £50,000 per annum, rising with inflation at 2% per year (excluding mortgage repayments).

- Life expectancy to age 90.

- The couple each fund £20,000 per year into ISAs.

- The non-working spouse contributes £3,600 per year (gross) to a stakeholder pension.

- From 2016, the partner pays £10,000 per annum (gross) into a pension (maximum contribution under new rules from April 2016).

- The couple purchased their main residence for £500,000 and it is now valued at £1m. They plan to repay the mortgage and the payments are £12,500 per annum.

- Investment returns are 5% (so real returns of 3% when inflation is considered) with charges at 1%.

DISCLAIMER

By necessity, this briefing can only provide a short overview and it is essential to seek professional advice before applying the contents of this article. This briefing does not constitute advice nor a recommendation relating to the acquisition or disposal of investments. No responsibility can be taken for any loss arising from action taken or refrained from on the basis of this publication. Details correct at time of writing.

Disclaimer

This article was previously published on Smith & Williamson prior to the launch of Evelyn Partners.